Since the introduction of open banking to the UK market in January 2018, it’s grown rapidly into a truly integrated system between banks, FinTechs and trusted third-parties. As of early 2026, UK open banking has over 16 million users, with high adoption among consumers and small businesses. Globally, open banking–based services are already used by well over 100 million customers, and the market is scaling fast across Europe and beyond.

It is now being implemented worldwide, with many other nations adopting similar standards for open banking integration. This is also leading to organizations re-thinking how the open banking mortgage process should work end-to-end.

The big thing about open banking is that it’s all based on access, integration, permissions and privacy, not all of which are clear.

Why Traditional Mortgage Operating Models Are Under Strain

The critical factors are always security and authentication, and it’s interesting that we now often have to pass several gateways to approve digital transactions. For example, I recently had to go through three verification steps for a simple transaction of less than Euro 100. This was because the merchant used Visa Click to Pay to verify the user; I then paid with Mastercard, which required a text message confirming it was me; and then a third step of opening the Mastercard bank app to re-verify that it was me and approve the payment.

If that's the friction on a simple Euro 100 payment, imagine what it looks like across a full mortgage application with dozens of checks running through different providers. Right now, the UK mortgage market is under real pressure. Affordability is stretched, first-time buyers are being priced out or delayed, and lenders are caught between tightening criteria and trying to keep volumes moving.

That makes it more important than ever that banks process, assess and approve mortgage applications. And that’s where open banking comes in.

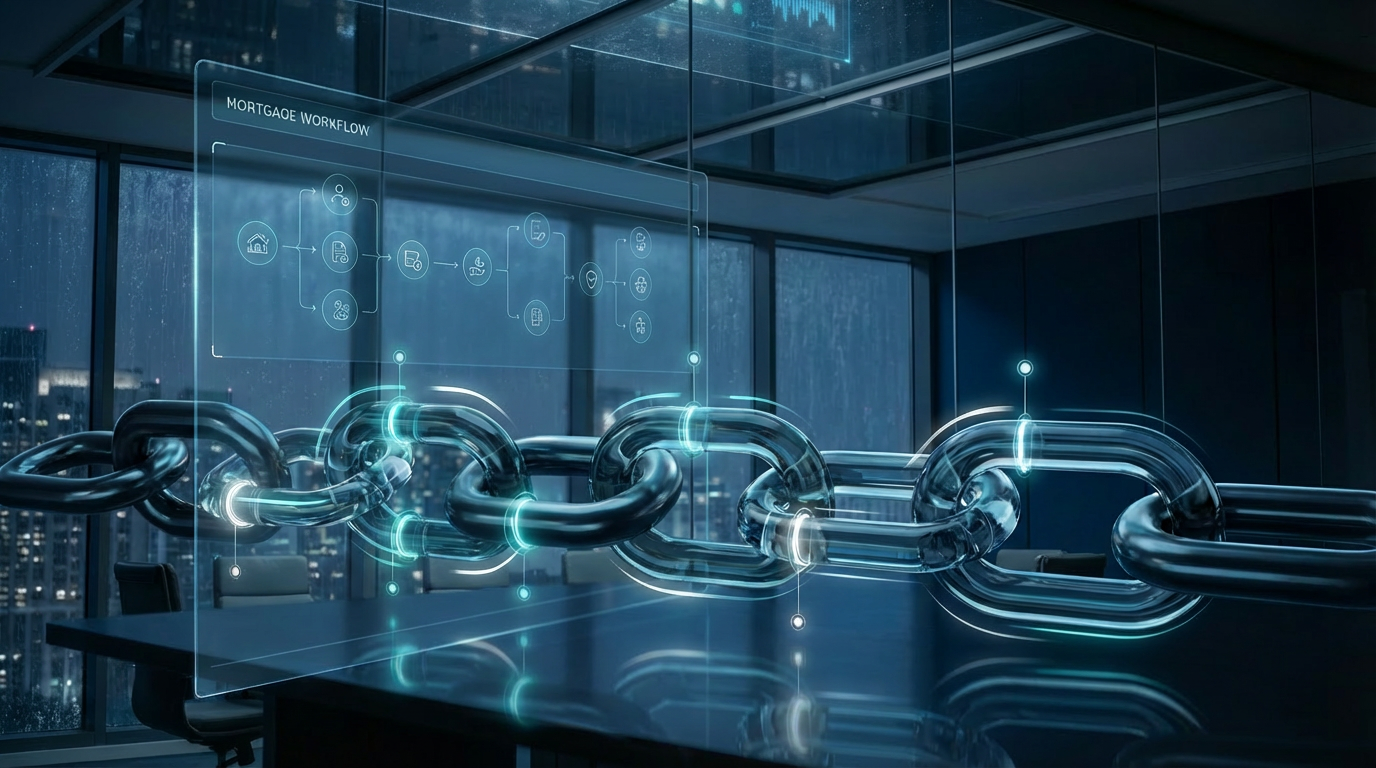

How Open Banking is Transforming Mortgage Processing

The good news is that we now have a broad ecosystem of APIs, trusted third-parties and more to ease these processes: Authentication, verification, credit checks, the lot. Industry estimates suggest that open banking API traffic is growing at double digit rates, with tens of billions of API calls now being made annually as banks expose more services to third-parties.

The bad news is that it is still clunky and chunky and doesn’t quite work as it should. More than this, everyone wants a piece of the action in the process. After all, if third-parties are not making money out of simplifying processes, who is?

This raises a key question for banks, as they need to be open to third-party integration, open banking, APIs and the new architectures of integration, but are they? Add the question around customer choice and costs, and you can see the dilemma.

What it really means is that the person responsible for partnerships, integration and technology within a traditional bank is no longer a CIO or Head of Data. It is an architect who operates as a conductor of an orchestra of technologies.

This is a brand-new role that replaces the old ways of just working with large tech firms to automate back-office systems. In those good old days, you typically worked with just one or two technology providers, whereas now we are talking about many, including the likes of Stripe, Adyen, PayPal, Monzo, Revolut, Wise, eToro and more. And nowhere is that orchestra more complex than in mortgage lending, where a true mortgage ecosystem banking model is emerging.

AI and Ecosystem Partnerships in Mortgage Lending

A mortgage involves many checks and balances from onboarding through evaluation, offer and completion. It’s an incredibly complex process that used to be handled internally by a bank from start to finish. Today, many of the checks and balances in that process are augmented by third-party providers, from credit checks to balance checks to checks on prior ownerships to checks on status, identity and more.

It’s worth noting that many of these additional checks aren’t just a technology story; they’re driven by tighter lending standards and more rigorous affordability assessments, particularly in the UK market. But open banking integration via APIs enables those checks to run without the process grinding to a halt. It no longer needs a huge internal underwriting process. It can actually be done in minutes through the ecosystem of technologies we use today. This is where mortgage lending digital transformation becomes visible to the customer: A complex, multi-step journey delivered as a seamless, largely invisible flow.

In other words, mortgage FinTech has transformed the home-buying process from a slow, paper-heavy, legacy system to an automated, digital-first system.

These solutions, including AI-driven mortgage underwriting, open banking data analysis and digital document verification, significantly reduce loan processing times from weeks to days, enhance the customer experience, and improve risk management and processing accuracy.

The Future: An Orchestrated Mortgage Operating Model

I've seen this orchestration challenge first-hand. Increasingly, banks are turning to operational partners such as WNS to coordinate partner-led workflows across the mortgage lifecycle — onboarding, verification, credit assessment and completion — so the entire process runs as a single operating model rather than a patchwork of disconnected handoffs.

All in all, it’s a game of checks and balances, and the open ecosystem of today’s technologies enables us to do this faster and more easily than ever before.

It is no different from the days of old, except that in the olden days, banks did all this themselves. Now, thousands can do it with them.

The big question for a bank is no longer just what technology to use; it’s who coordinates it all.

When you’ve got credit checks running through one provider, identity verification through another, affordability assessments through a third and your own internal teams trying to keep it all joined up, the real challenge isn’t the technology but the orchestration. Who makes the whole thing work as one process rather than twenty? That is the real test of whether your mortgage operating model is truly built for open banking.

About the Author

Chris Skinner

Independent Commentator on

Financial Markets & FinTech

Chris is an independent commentator on financial markets, known for his blog TheFinanser.com and as the author of the bestselling book Digital Bank. He chairs the Financial Services Club and is recognized as one of the most influential voices in banking and FinTech.

FAQs

1. How can open banking actually improve mortgage approval timelines for our bank?

Open banking enables real-time access to verified financial data through APIs, reducing dependency on manual document collection and validation. This significantly accelerates underwriting, allowing banks to move from weeks to days in processing while improving decision accuracy.

2. What are the key risks in adopting an open banking-based mortgage model?

The primary risks include data security, regulatory compliance, and managing multiple third-party integrations. However, with strong governance, API security frameworks, and partner oversight, these risks can be effectively mitigated while unlocking operational efficiency.

3. How do we manage multiple fintech partners without increasing operational complexity?

Success depends on establishing an orchestration layer that integrates and manages all third-party services seamlessly. Instead of fragmented workflows, banks need a unified operating model that ensures coordination across credit checks, identity verification, and affordability assessments.

4. What role does AI play in improving mortgage underwriting and decisioning?

AI enhances underwriting by analyzing large volumes of financial and behavioral data quickly and accurately. It improves risk assessment, detects anomalies, and enables more personalized lending decisions, while also reducing manual intervention and errors.

5. How can we ensure a consistent customer experience across a multi-partner ecosystem?

A well-designed digital journey with centralized orchestration ensures that customers experience a seamless process despite multiple backend integrations. Standardized workflows, real-time updates, and minimal friction points are critical to maintaining a consistent experience.

6. Is it more effective to build these capabilities in-house or partner with external providers?

While building in-house offers control, it often slows down innovation and scalability. Partnering with specialized providers allows banks to access proven capabilities, accelerate transformation, and focus internal teams on strategic priorities rather than operational execution.

7. How do we measure ROI from transforming our mortgage operating model?

ROI can be measured through reduced processing time, lower operational costs, improved approval rates, higher customer satisfaction, and increased loan volumes. Additionally, faster turnaround times directly impact revenue realization and competitive positioning.