“Change & Synergies” – Critical Success Factors for Insurers in Today’s Regulatory Environment

Two directives that will soon change the face of the insurance industry in the European Economic Area are Solvency II and IFRS 4 Phase II. While Solvency II focuses on establishing a single common regulatory framework to maintain capital adequacy and risk management standards, the International Accounting Standards Board (IASB) aims to “develop a single set of high quality, understandable, enforceable and globally accepted financial reporting standards based upon clearly articulated principles”, with IFRS 4.

Currently, reporting standards followed by the insurance industry are divergent, and this leads to discrepancies and confusion when accounting results from different geographies are compared. Solvency II and IFRS 4 aim to improve transparency and comparability from a regulatory and accounting perspective, respectively.

One directive (Solvency II) is a regulation and the other (IFRS 4) a financial reporting standard; but there is considerable overlap between the two and although implementation of both Solvency II and IFRS 4 could occur within a gap of a year anda- half or two, it would make great business sense for European insurers to take a coordinated approach in preparing to meet both directives.

Creating synergies and taking a coordinated approach will help reduce implementation costs; improve governance; and lend confidence to insurers currently concerned about meeting Solvency II and IFRS 4 within a short period of time. From an organizational perspective, the impact of both Solvency II and IFRS 4 (Phase II) are likely to be felt on the data and systems; reporting and disclosure mechanism; governance policies and protocols; and finally the people in the organization.

The multi-level impact that Solvency II and IFRS 4 are likely to have on European insurers calls for initiating change and more importantly creating synergies between the overlaps (in Solvency II & IFRS 4) in equipping organizational resources (reporting mechanisms, systems and data, policies and protocols and people) in meeting these two directives.

Solvency II & IFRS 4 Phase II – Differences & Similarities:

Differences

Both the differences and similarities are important for the insurer, from an implementation perspective. First, a look at the differences:

- The first difference is clearly based on the two divergent objectives that these two directives aim to achieve. Solvency II will lead to competitiveness of the products in terms of their pricing and features offered by insurers, with its focus mainly on solvency capital requirement and enhanced level of policyholder protection. IFRS 4 on the other hand, aims to apply uniform accounting standards for all types of insurance contracts and also to reduce the gap between standards followed in insurance. IFRS 4 reporting will be more transparent due to stringent disclosure requirements.

- The next difference is at the level of restrictions on liquidity premium. While Solvency II measures have specified the risk-free rate as well as liquidity premium (available in QIS5 document), under IFRS 4, there is no such restriction on liquidity premium.

- The next difference is at the level of restrictions on liquidity premium. While Solvency II measures have specified the risk-free rate as well as liquidity premium (available in QIS5 document), under IFRS 4, there is no such restriction on liquidity premium.

- The third difference is that although the principles-based approach will be adopted in both directives, Solvency II measures are more prescriptive and comprehensive as compared to IFRS 4.

- Profits will be recognized immediately at the inception under Solvency II, while under IFRS 4 profits will be recognized over the period of the insurance contract.

- Finally, unlike Solvency II, general overheads will not be allowed in cash flows under IFRS 4 Phase II.

Similarities

While there are differences between Solvency II and IFRS 4, there are certain similarities between the two frameworks that insurers will need to carefully consider while developing an approach for implementation of both the directives. A look at the similarities:

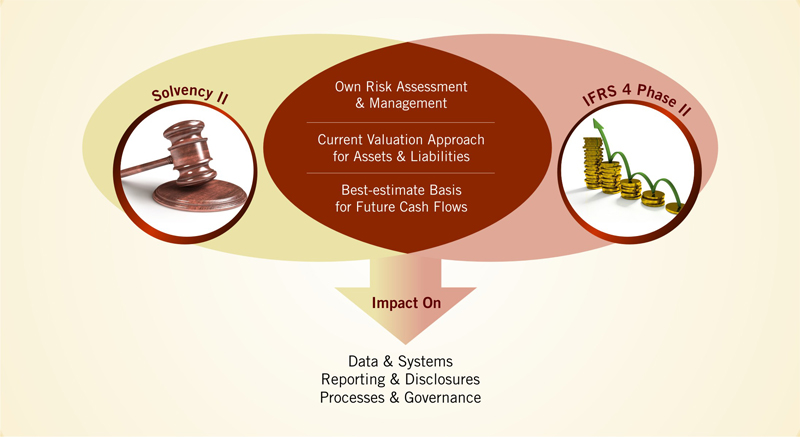

- Solvency II and the Phase II of IFRS 4 emphasize on the insurer’s own assessment and management of risks facing the business. In both directives, there is a departure from the narrow and prescriptive rules and adoption of a broader and more risk- and principles-based approach to regulation.

- Under both Solvency II and IFRS 4, asset and liabilities are likely to use a current valuation approach, which is expected to increase volatility on financial statements in comparison to current standards.

- Under Solvency II and IFRS 4, best-estimate basis is used in expected future cash flows (unbiased, probability weighted estimate of cash outflows minus cash inflows). Discount rate used is the sum of risk-free rate and liquidity premium.

Similarities among Both Directives Call for a Coordinated Approach:

The real ‘time’ convergence of Solvency II and IFRS 4 Phase II seems unlikely. Solvency is likely to be implemented at least a couple of years ahead of IFRS 4 Phase II. However, for insurers, it makes complete business sense to take a coordinated approach for the implementation of both directives, given the significant overlaps in the requirements for Solvency II and IFRS 4 Phase II.

Impact on Data & Systems

Solvency II and IFRS 4 Phase II have similar data requirements. Both require insurers to invest in data quality, control and management. However there will be differences in definition of portfolio and contract boundaries. A major requirement will be to ensure that the organization’s systems are flexible enough to factor in these differences in inputs to cash flows between Solvency II and IFRS 4 Phase II.

Impact on Processes & Governance

Under IFRS 4 Phase II, accounting policies will need to be standardized and insurers will need to ensure that the processes developed to comply with IFRS 4 Phase II, are auditable. On the other hand, insurers will need to conform to the governance and control framework promulgated in the Pillar 2 of Solvency II, in terms of policies, assumptions and calculation methods.

Impact on Reporting & Disclosures

Insurers will need to take care when planning a common approach to reporting and regulatory disclosure standards for both sets of requirements. In spite of similarities between IFRS 4 Phase II and the Pillar 3 of Solvency II, there will be challenges in implementation. There could be inconsistencies in the way an organization’s risk profile is reported under IFRS 4 vis-à-vis Solvency II. It will require a mature understanding of the insurance business as well as accounting, reporting and disclosures for a smooth implementation.

Partner with the Expert:

With the European insurance industry, heading towards meeting two crucial regulatory / reporting milestones, the role of a partner with a keen understanding of the insurance business and accounting, reporting and disclosures will be crucial in determining business success in the post-Solvency II and IFRS 4 Phase II regime.

WNS is a leading provider of global Business Process Outsourcing (BPO) services with long-standing experience in insurance processes for leading insurers across the world.

WNS plays an active role for supporting the clients in the following areas:

- Actuarial Systems Support: WNS has rich experience and expertise in supporting the transformation of actuarial systems, and helps clients comply with ever-changing regulatory requirements. WNS provides expertise in data management (data extraction, cleaning and validation), model development, automation and optimization (to reduce the runtime by deletion of redundant variables and indicator expressions and using macros), regular maintenance and Quality Control (Unit / system and Regression testing, adequate documentation).

- Solvency II support: Our experienced team assists clients in accelerating their Solvency II program by providing expertise in areas such as Actuarial model development (used in providing information for internal management purposes), Information Technology and data (to establish systems, processes and controls for effective risk management, and to help implementation requirements across the three pillars of Solvency II framework), risk management (support for developing ORSA framework, embedding its implementation at a management and operational level), Reporting and Disclosure Requirements (to comply with Pillar 3 regulatory requirements).

- Financial Reporting and Measurement: With a strong knowledge of industry best practices and emerging financial reporting standards, WNS works closely with clients to simplify, rationalize and streamline their reporting processes. We provide them with tools for ensuring accurate and efficient reporting. This typically involves end-to-end delivery of Actuarial reporting, experience analysis (lapse / persistency, mortality / morbidity), production of results (basis generation, production runs for in-force business, stress testing and extraction of results), stochastic runs for with-profit business, Analysis of Change (AOC) (impact on key variables, including present value of future profit, margins, asset share and cost of guarantees) and consolidation and submission of regulatory forms.

WNS in Insurance:

WNS is a leader in insurance-specific business services with a comprehensive range of solutions in Property & Casualty; Life, Pensions & Annuity to address end-to-end needs of global insurers across the industry value chain. Our bouquet of insurance solutions include new business management, policy set up and changes, premium management, claims management, payments management, agency & distribution management, support services and actuarial services.

Backed by a strong foundation of Technology, Analytics and mature Process Services, our industry-leading and proprietary solutions such as ProClaim, Elixir, TCP Life Systems, STG Suite and the WNS CoE for Actuarial Services create enhanced value for our clients from the insurance domain in every corner of the world. We have over 8,500 domain experts, serving our clients in the global insurance industry.